Treasury

THE CORONAVIRUS ACT 2020

FUNCTIONS OF HER MAJESTY’S REVENUE AND CUSTOMS (CORONAVIRUS JOB RETENTION SCHEME) DIRECTION

The Treasury, in exercise of the powers conferred by sections 71 and 76 of the Coronavirus Act 2020, give the following direction:

1. This direction applies to Her Majesty’s Revenue and Customs.

2. This direction modifies the effect of the Coronavirus Job Retention Scheme for which Her Majesty’s Revenue and Customs is required to be responsible for the payment and management of amounts payable under the scheme set out in the Schedule to the direction made on 15 April 2020 by the Treasury in exercise of the powers conferred by sections 71 and 76 of the Coronavirus Act 2020 as modified by the further direction made in exercise of those powers on 20 May 2020 (“the original CJRS directions”).

3. The original CJRS directions continue to have effect but are modified as set out in the Schedule to this direction.

Signed by the Chancellor of the Exchequer

Her Majesty’s Treasury

25 June 2020

SCHEDULE

CORONAVIRUS JOB RETENTION SCHEME

Introduction

1.1 This Schedule sets out modifications to the scheme known as the Coronavirus Job Retention Scheme (“CJRS”) established by the original CJRS directions.

1.2 In particular-

(a) part 1 of this Schedule makes provision in respect of CJRS as set out in the original CJRS directions, and

(b) part 2 of this Schedule makes provision in respect of CJRS for the period beginning on 1 July 2020 and ending on 31 October 2020.

1.3 The provision made by part 2 of this Schedule in relation to CJRS is without prejudice to any matter in connection with the provision made by the original CJRS directions or part 1 of this Schedule.

1.4 Except as necessary to give effect to CJRS as set out in part 2 of this Schedule, the provision made by the original CJRS directions and part 1 of this Schedule is without prejudice to any matter in connection with the provision made by part 2 of this Schedule.

Purpose of CJRS

2.1 The purpose of CJRS is to provide for payments to be made to employers on a claim made in respect of them incurring costs of employment in respect of employees who are within the scope of CJRS arising from the health, social and economic emergency in the United Kingdom resulting from coronavirus and coronavirus disease.

2.2 Integral to the purpose of CJRS is that the amounts paid to an employer pursuant to a CJRS claim are used by the employer to continue the employment of employees in respect of whom the CJRS claim is made whose employment activities have been adversely affected by the coronavirus and coronavirus disease or the measures taken to prevent or limit its further transmission.

2.3 CJRS claims must be made in such form and manner and contain such information as HMRC may require at any time (whether before or after payment of the claim) to establish entitlement to payment under CJRS.

2.4 Before making payment of a CJRS claim, HMRC must, by publicly available guidance, other publication generally available to the public, or such other means considered appropriate by HMRC, inform a person making a CJRS claim that, by making the claim, the person making the claim accepts that-

(a) a payment made pursuant to such claim is made only for the purpose of CJRS (and, in particular, as provided for by paragraph 2.2), and

(b) the payment must be returned to HMRC immediately upon the person making the CJRS claim becoming unwilling or unable to use the payment for the purpose of CJRS.

2.5 No CJRS claim may be made in respect of an employee if it is abusive or is otherwise contrary to the exceptional purpose of CJRS.

PART 1

PROVISION FOR CJRS CLAIMS AS SET OUT IN THE ORIGINAL CJRS DIRECTIONS (CJRS HAVING EFFECT FROM 1 MARCH 2020 TO 30 JUNE 2020)

Time limit for making CJRS claims as set out in the original CJRS directions

3. A CJRS claim-

(a) must not be made in respect of a time occurring after 30 June 2020, and

(b) must not be made after 31 July 2020.

Furloughed employees

4. For the purposes of a CJRS claim, it does not matter if the period for which an employee has ceased (or will have ceased) all work (whether directly or indirectly) for the employee’s employer (or a person connected with the employee’s employer) for 21 calendar days or more ends after 30 June 2020 (but no CJRS claim may be made in respect of the period after that date (see paragraph 3(a)).

Succession to a business

5.1 Paragraph 5.2 applies in relation to CJRS claims made pursuant to paragraphs 9.1 and 10.2 of the Schedule to the second CJRS direction in respect of the remaining CJRS period.

5.2 Where this paragraph applies, paragraph 6.1(b) of the Schedule to the second CJRS direction must be construed as if the references to 21 calendar days in those paragraphs were references to the remaining CJRS period. 5.3 The remaining CJRS period is the period-

(a) beginning immediately after a relevant transfer occurring on or after 10 June 2020, and

(b) ending on 30 June 2020.

Definitions etc.

6. For the purposes of part 1 of this Schedule-

(a) “CJRS claim” means a claim made in accordance with the original CJRS directions;

(b) “relevant transfer” has the same meaning as it does in paragraph 9.12(b) of the schedule to the second CJRS direction;

(c) “second CJRS direction” means the direction made on 20 May 2020 by the Treasury in exercise of the powers conferred by sections 71 and 76 of the Coronavirus Act 2020.

PART 2

PROVISION IN RESPECT OF CJRS FOR THE PERIOD BEGINNING ON 1 JULY 2020 AND ENDING ON 31 OCTOBER 2020

Entitlement to make a CJRS claim

7. A CJRS claim may be made by a qualifying employer in respect of an employee who is a flexibly-furloughed employee in a CJRS claim period.

Qualifying employers

8.1 An employer is a qualifying employer if-

(a) the employer has a qualifying PAYE scheme, and

(b) the employer has made a qualifying CJRS claim on or before 31 July 2020.

8.2 An employer has a qualifying PAYE scheme if-

(a) at the time of making the CJRS claim, the employer has a PAYE scheme registered on HMRC’s real time information system for PAYE, and

(b) that scheme was registered as described in paragraph 8.2(a) on or before 19 March 2020.

8.3 A qualifying CJRS claim is a claim-

(a) made in accordance with the original CJRS directions, and

(b) made in respect of an employee who ceased all work (whether directly or indirectly) for the employer (or a person connected with the employer) for a period of 21 calendar days or more beginning on or before 10 June 2020.

Employers with more than one PAYE scheme

9. If an employer has more than one qualifying PAYE scheme-

(a) the employer must make a separate CJRS claim in relation to each scheme, and

(b) the amount of any payment under CJRS will be calculated separately in relation to each scheme.

Flexibly-furloughed employees

10.1 An employee is a flexibly-furloughed employee in a CJRS claim period if-

(a) the employee is a qualifying employee for the purposes of CJRS,

(b) the employee has been instructed by the employer-

(i) to do no work in relation to their employment during a CJRS claim period, or

(ii) not to work the full amount of the employee’s usual hours in relation to their employment during a CJRS claim period,

(c) the employee-

(i) does no work in relation to their employment during the CJRS claim period, or

(ii) does not work the full amount of the employee’s usual hours in relation to their employment during the CJRS claim period,

(d) the instruction is given by reason of circumstances arising as a result of coronavirus or coronavirus disease or measures taken to prevent or limit its further transmission, and

(e) there is an agreement in accordance with paragraph 13 having effect for the period covered by the CJRS claim period.

10.2 An employee is a qualifying employee for the purposes of CJRS if-

(a) paragraph 10.3 applies in relation to the employee,

(b) the employee is a family leave returner (see paragraphs 11.1 and 11.2), or

(c) the employee is an armed forces reservist employee (see paragraph 12).

10.3 This paragraph applies in relation to an employee if-

(a) on or before 31 July 2020, the employee’s employer makes a CJRS claim in accordance with the original CJRS directions in respect of the employee for a period ending on or before 30 June 2020, and

(b) the employee ceased all work (whether directly or indirectly) for the employer (or a person connected with the employer) for a period of 21 calendar days or more beginning on or before 10 June 2020.

Family leave returner

11.1 A family leave returner is an employee-

(a) to whom paragraph 10.3 does not apply,

(b) who has taken a period of family leave-

(i) beginning on or before 10 June 2020, and

(ii) ending after 10 June 2020,

(c) to whom the employer made a payment of earnings in the tax year 2019-20 which is shown in a return under Schedule A1 to the PAYE Regulations that is made on or before a day that is a relevant CJRS day, and

(d) in relation to whom the employer has not reported a date of cessation of employment on or before that day.

11.2 An employee takes a period of family leave at a time when the employee is taking a period of leave to which the employee is entitled (including a period during which an employer must not permit an employee to work) by virtue of-

(a) Chapters 1 (maternity leave), 1A (adoption leave), 1B (shared parental leave), 3 (paternity leave) and 4 (parental bereavement leave) of Part 8 of the Employment Rights Act 1996,

(b) Chapters 1 (maternity leave), 1A (adoption leave), 1B (shared parental leave) and 3 (paternity leave) of Part 9 of the Employment Rights (Northern Ireland) Order 1996, or

(c) any provision made for Northern Ireland corresponding to Chapter 4 (parental bereavement leave) of Part 8 of the Employment Rights Act 1996.

Armed forces reservist employee

12.1 An armed forces reservist employee is an employee-

(a) to whom paragraph 10.3 does not apply,

(b) who, (as an officer or a man enlisted, re-engaged or recalled into service in the reserve forces for the purposes of the Reserve Forces Act 1996), has been called out or recalled for service in accordance with that Act for a period-

(i) beginning on or before 10 June 2020, and

(ii) ending after 10 June 2020,

(c) to whom the employer made a payment of earnings in the tax year 2019-20 which is shown in a return under Schedule A1 to the PAYE Regulations that is made on or before a day that is a relevant CJRS day, and

(d) in relation to whom the employer has not reported a date of cessation of employment on or before that day.

12.2 References in paragraph 12.1 to “officer”, “man”, “enlisted”, re-engaged”, “recalled”, “service”, “reserve forces” and “called out” have the same meanings as they do in the Reserve Forces Act 1996.

Agreement between employer and employee

13. An agreement is in accordance with this paragraph if-

(a) the employer and employee have agreed (such agreement may be made by means of a collective agreement between the employer and a trade union) that-

(i) the employee will do no work in relation to their employment, or

(ii) the employee will not work the full amount of the employee’s usual hours in relation to their employment,

(b) the agreement (including a collective agreement) specifies the main terms and conditions upon which the employee -

(i) will do no work in relation to their employment, or

(ii) will not work the full amount of the employee’s usual hours in relation to their employment,

(c) the agreement (including a collective agreement)-

(i) is made before the beginning of the period to which the CJRS claim relates (but may subsequently be varied to reflect any variation agreed between the employer and employee during the period to which the CJRS claim relates),

(ii) is incorporated (expressly or impliedly) in the employee’s contract, and

(iii) is made in writing or confirmed in writing by the employer (such agreement or confirmation may be in an electronic form such as an email), and

(d) the agreement (including a collective agreement) or confirmation is retained by the employer until at least 30 June 2025.

CJRS claim periods

14.1 A CJRS claim may only be made in respect of a CJRS claim period.

14.2 A CJRS claim period is a period that-

(a) begins and ends in the same CJRS calendar month, and

(b) relates to-

(i) a period of 7 or more consecutive days, or

(ii) an orphan period.

14.3 An orphan period is a period of no more than 6 consecutive days that-

(a) begins on the first day of a CJRS calendar month, or

(b) ends on the last day of a CJRS calendar month.

14.4 A CJRS claim in relation to an employee may only be made in respect of an orphan period if the employer also makes a CJRS claim in respect of that employee for a CJRS claim period ending immediately before that orphan period.

14.5 A CJRS claim must not be made if the CJRS claim period of the claim would include a day that is not a permitted CJRS day.

14.6 A day is a permitted CJRS day if that day-

(a) falls in a period that is (or will be) covered by a CJRS claim period (“relevant CJRS claim period”), and

(b) does not fall in a period covered by a CJRS claim period that-

(i) begins on a different day to the day on which the relevant CJRS claim period begins, or

(ii) ends on a different day to the day on which the relevant CJRS claim period ends.

14.7 Paragraph 14.8 applies where-

(i) a return to work day (see paragraphs 15.8 to 15.11) of a returning employee occurs in a period that is not an orphan period, and

(ii) the employer reasonably considers that the making of a CJRS claim in respect of the returning employee for a CJRS claim period beginning on the return to work day would be simplified if it is made for a period of less than 7 consecutive days.

14.8 Where this paragraph applies, a CJRS claim may be made in respect of the returning employee for a CJRS claim period of less than 7 consecutive days (“initial CJRS claim period”) if the employer makes a CJRS claim in respect of that employee for a CJRS claim period beginning immediately after the initial CJRS claim period.

14.9 In relation to the initial CJRS claim period described in paragraph 14.8, paragraph 14.5 and 14.6 apply as if paragraph 14.6(b)(i) were omitted.

14.10 The CJRS calendar months are-

(a) July 2020;

(b) August 2020;

(c) September 2020;

(d) October 2020.

Maximum number of employees that may be claimed for in a CJRS claim

15.1 A CJRS claim must not be made by an employer in respect of more than the number of allowable claimed-for employees for a CJRS claim.

15.2 An employee is a claimed-for employee if a CJRS claim is made in respect of the employee for all or part of a CJRS claim period.

15.3 An employee is a relevant claimed-for employee if a relevant CJRS claim has been made in respect of the employee for all or part of the period covered by that claim.

15.4 A CJRS claim is a relevant CJRS claim if it is made in accordance with the original CJRS directions.

15.5 The number of allowable claimed-for employees for a CJRS claim is the high-watermark number.

15.6 The high-watermark number is the number of relevant claimed-for employees for a relevant CJRS claim that is a high-watermark claim.

15.7 A relevant CJRS claim is a high-watermark claim if the number of relevant claimed-for employees for that claim is not lower than the number of relevant claimed-for employees for any other relevant CJRS claim.

15.8 For the purposes of determining the number of allowable claimed-for employees in respect of a CJRS claim for a CJRS claim period that includes a day falling on or after a return to work day of a returning employee, paragraphs 15.1 to 15.7 apply as if the returning employee falls as a relevant claimed-for employee in relation to all relevant CJRS claims made by the employer.

15.9 An employee is a returning employee if-

(a) the employee is an armed forces reservist employee, or

(b) the employee is a family leave returner.

15.10 A day is a return to work day of a returning employee if-

(a) that day falls after 10 June 2020, and

(b) that day is the first day the returning employee undertakes work for the employer after the relevant event in respect of that employee.

15.11 The relevant event in respect of a family leave returner is the ending of a period of family leave (see paragraph 11.1(b)).

15.12 The relevant event in respect of an armed forces reservist employee is the ending of the employee’s called out service after 10 June 2020 (see paragraph 12.1(c)).

15.13 Paragraph 15.8 must not be construed as requiring a CJRS claim to be made in respect of a returning employee.

Qualifying costs

16.1 The costs of employment in respect of which an employer may make a CJRS claim are costs which-

(a) relate to an employee who is a flexibly-furloughed employee for the CJRS claim period,

(b) relate to the payment of earnings to the employee during that period, and

(c) meet the condition in paragraph 16.2 in relation to the employee’s furloughed hours occurring in the CJRS claim period.

16.2 The condition referred to in paragraph 16.1(c) is that the amount payable to the employee in relation to the employee’s furloughed hours occurring in the CJRS claim period is an amount equal to or more than an amount determined in accordance with-

(a) the formula set out in paragraph 16.3, or

(b) if the amount payable to the employee in relation to the employee’s furloughed hours occurring in the CJRS claim period is less than the amount determined in accordance with the formula set out paragraph 16.3, the formula set out in paragraph 16.4.

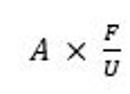

16.3 The formula referred to in paragraph 16.2(a) is-

.

.

16.4 The formula referred to in paragraph 16.2(b) is-

16.5 For the purposes of paragraphs 16.3 and 16.4-

(a) A is-

(i) £2500 if the CJRS claim period covers the whole of the CJRS calendar month to which the CJRS claim relates, or

(ii) if the CJRS claim period is for a period that does not cover the whole of the CJRS calendar month to which the claim relates, the appropriate pro-rata;

(b) B is the amount which is 80% of the employee’s reference salary attributable to the CJRS claim period of the CJRS claim;

(c) F is the number of furloughed hours in the CJRS claim period;

(d) U is the number of usual hours in the CJRS claim period.

16.6 Paragraph 16.7 applies where the period of time covered by a CJRS claim period in respect of an employee is not the same as, or comparable to, the period of time covered by the salary period by reference to which the employee’s reference salary is determined in accordance with paragraph 19.2 or 20.1.

16.7 For the purposes of determining the amount B (see paragraph 16.5(b)), the employee’s reference salary must be adjusted proportionately to ensure that the reference salary fairly reflects the proportion attributable to the period covered by the CJRS claim period.

16.8 For the purposes of paragraph 16.6, the period of time covered by a CJRS claim period and the period of time covered by a salary period are comparable if-

(a) the CJRS claim period is for the whole of a CJRS month, and

(b) the period of time covered by the salary period is no less than 28 days and no more than 31 days.

16.9 The condition in paragraph 16.2 is not met if the amount payable in respect of the employee is not paid to the employee.

Simplification of a CJRS claim allowable where an employee does no work in a CJRS claim period

17.1 Where an employee does no work in a CJRS claim period, paragraph 16.2 may be applied as if the condition in that paragraph required the amount payable to the employee in respect of the CJRS claim period to be an amount equal to or more than an amount determined in accordance with-

(a) the amount A (see paragraph 16.5(a)), or

(b) the amount B (see paragraph 16.5(b)) if the amount payable in respect of the CJRS claim period is less than the amount A.

17.2 Where paragraph 16.2 is applied as described in paragraph 17.1, the provision made by Part 2 of this Schedule (in particular, paragraphs 16.5 to 16.8, 30 and 31.1 to 31.4) must be construed accordingly.

Reference salary

18. The reference salary of an employee must be determined in accordance with-

(a) paragraphs 19.1 to 19.8 and 21.1 to 21.7 if the employee is a fixed rate employee, and

(b) paragraphs 20.1 and 20.2 and 21.1 to 21.7 if the employee is not a fixed rate employee.

Reference salary – fixed rate employees

19.1 A person is a fixed rate employee if- (a) the person is-

(i) an employee, or

(ii) treated as an employee for the purposes of CJRS by virtue of paragraph 41.3(a) (member of a limited liability partnership),

(b) the person is entitled under their contract to be paid an annual salary,

(c) the person is entitled under their contract to be paid that salary in respect of a number of hours in a year whether those hours are specified in or ascertained in accordance with their contract (“the basic hours”),

(d) the person is not entitled under their contract to a payment in respect of the basic hours other than an annual salary,

(e) the person is entitled under their contract to be paid, where practicable and regardless of the number of hours actually worked in a particular week or month in equal weekly, multiple of weeks or monthly instalments, and

(f) the basic hours worked in a salary period do not normally vary according to business, economic or agricultural seasonal considerations.

19.2 The reference salary of a fixed rate employee is the amount payable to the employee in the latest salary period ending on or before 19 March 2020 (but disregarding anything which is not regular salary or wages as described in paragraph 21.1).

19.3 In paragraph 19.1, “contract” means a legally enforceable agreement as described in paragraph 21.2(b).

19.4 In respect of a fixed rate employee, where a period by reference to which the reference salary is determinable (“reference salary period”) includes a period of unpaid sabbatical or unpaid leave (“unpaid period”), the reference salary must be determined on the basis of what would have been paid to the employee during the unpaid period if the sabbatical or leave had been granted on the same terms as the employee’s paid leave during the reference salary period taking account of the matters described in paragraphs 19.5 to 19.8 as are appropriate.

19.5 In paragraph 19.4-

(a) the reference to the terms of an employee’s paid leave during a reference salary period is a reference to the terms applying in respect of the annual leave to which the employee would have been entitled to be paid pursuant to regulation 16 of the Working Time Regulations 1998 or regulation 20 of the Working Time (Northern Ireland) Regulations 2016 (“paid annual leave”) if the period of unpaid leave had been a period of paid annual leave;

(b) the references to unpaid sabbatical and unpaid leave also include references to-

(i) statutory payment leave, and

(ii) reduced rate paid leave.

19.6 In paragraph 19.5(b)(i), “statutory payment leave” means a period of leave-

(a) in respect of which statutory sick pay or any of the statutory payments specified in paragraph 32.2 is in payment or due to be paid, or

(b) which is a period of shared parental leave as provided for by regulations made pursuant to sections 75E and 75G of the Employment Rights Act 1996 or articles 107E and 107G of the Employment Rights (Northern Ireland) Order 1996 (whether or not statutory shared parental pay described in paragraph 32.2(d) is in payment or due to be paid in respect of that period).

19.7 In paragraph 19.5(b)(ii), “reduced rate paid leave” means a period of leave granted immediately following the ending of a period of statutory payment leave on terms that are not the terms which would have applied to that period of leave if the leave had been granted on the same terms that would have applied if the leave had been a part of the employee’s statutory leave entitlement.

19.8 For the purposes of paragraph 19.6(a), it does not matter if, by virtue of a legally enforceable agreement, understanding, scheme, transaction or series of transactions, the person described in that paragraph has been paid an amount in excess of the amount otherwise payable by way of statutory sick pay or the statutory payments specified in paragraph 32.2 to which the statutory payment leave relates.

Reference salary – employees other than fixed rate employees

20.1 In relation to an employee who is not a fixed rate employee, the reference salary of an employee or a person treated as an employee for the purposes of CJRS by virtue of paragraph 41.3(a) (member of a limited liability partnership) is the greater of-

(a) the average monthly (or daily or other appropriate pro-rata) amount payable to the employee in the period comprising the tax year 2019-20 (or, if less, the period of employment) before the period of furlough began, and

(b) the amount earned by the employee in the corresponding calendar period in the previous year.

20.2 The period of time by reference to which an employee’s reference salary is determined in accordance with paragraph 20.1 must be treated as the salary period by reference to which the employee’s reference salary is determined for the purposes of paragraphs 16.6 to 16.8.

Reference salary – general provisions

21.1 The following must not be included in the calculation of an employee’s reference salary for the purposes of paragraphs 19.2 and 20.1-

(a) benefits in kind;

(b) anything provided or made available in lieu of a cash payment otherwise payable to the employee (including salary sacrifice schemes);

(c) anything which is not regular salary or wages.

21.2 In paragraph 21.1(c) “regular” in relation to salary or wages means so much of the amount of the salary or wages as-

(a) cannot vary according to a relevant matter except where the variation in the amount arises from a non-discretionary payment (see paragraph 21.4), and

(b) arises from a legally enforceable agreement, understanding, scheme, transaction or series of transactions.

21.3 For the purposes of paragraph 21.2(a), the following are relevant matters-

(a) the performance of or any part of any business of the employer or any business of a person connected with the employer;

(b) the contribution made by the employee to the performance of, or any part of any business;

(c) the performance by the employee of any duties of the employment;

(d) any similar considerations or otherwise payable at the discretion of the employer or any other person (such as a gratuity).

21.4 A variation in an amount of wages or salary arises from a non-discretionary payment only if-

(a) the payment-

(i) is in respect of overtime, fees, commissions or a piece rate,

(ii) is made in recognition of the employee undertaking additional or exceptional responsibilities,

(iii) is made in recognition of the circumstances in which the employee undertakes the employee’s duties or time when they are undertaken, or

(iv) is made in recognition of other matters similar to those described in paragraph 21.4(a)(i) to (iii), and

(b) a legally enforceable agreement, understanding, scheme, transaction or series of transactions prescribe the method of calculating the amount of wages or salary payable in respect of the payment (whether or not that method involves the exercise of discretion by the employer or a person connected with the employer).

21.5 In calculating an employee’s reference salary in accordance with paragraph 19.2 or 20.1 in the case of a person (“P”) treated as an employee for the purposes of CJRS by virtue of paragraph 41.3(a) (member of a limited liability partnership) then, in addition to the matters described in paragraphs 21.1 to 21.3, no account is to be taken of an amount payable to P unless, by virtue of arrangements described in section 863B(5) of the Income Tax (Trading and Other Income) Act 2005, that amount-

(a) is fixed,

(b) is variable, but is varied without reference to the overall amount of the profits or losses of the limited liability partnership, or

(c) is not, in practice, affected by the overall amount of those profits or losses.

21.6 Where paragraph 21.7 applies, the sum of the original payment described in paragraph 21.7(a) and the further amount described in paragraph 21.7(c) must be treated as having been paid at the time of the payment of the original payment for the purposes of paragraph 16.2.

21.7 This paragraph applies where-

(a) an amount by way of wages or salary is paid in respect of a period of employment (“the original payment”) to an employee,

(b) the original payment is less than the amount required by paragraph 16.2 for the purpose of claiming CJRS,

(c) the employer has paid (or intends to pay within a reasonable period after receiving the payment claimed under CJRS) the employee a further amount (“the further amount”) in respect of the period of employment to which the original payment relates, and

(d) the sum of the original payment and the further amount meets the requirements of paragraph 16.2.

CJRS claim period – meaning of usual hours

22.1 The usual hours of an employee (whether or not the employee is a fixed rate employee) for a CJRS claim period must be determined-

(a) on the fixed hours basis if paragraph 22.2 applies in relation to the employee;

(b) on the variable hours basis in any other case.

22.2 This paragraph applies in relation to an employee whose contract-

(a) requires the employee to work a specific number of hours over a period of time prescribed by the contract, and

(b) does not require the employee’s pay in respect of the period of time prescribed by the contract to vary according to the number of hours actually worked in that period.

22.3 References to an employee’s contract in paragraphs 22.2, 23.4, 23.5, 26.4, 26.5 and 27.8 are to a legally enforceable agreement as described in paragraph 21.2(b).

CJRS claim period – usual hours – fixed hours basis

23.1 The formula in paragraph 23.2 applies to determine the usual hours for a CJRS claim period in respect of an employee whose usual hours must be determined on the fixed hours basis.

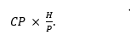

23.2 The formula referred to in paragraph 23.1 is-

23.3 For the purposes of paragraph 23.2-

(a) CP is the number of calendar days covered by the CJRS claim period;

(b) H is the number of working hours of the relevant repeating shift pattern;

(c) P is the number of calendar days covered by that repeating shift pattern.

23.4 A repeating shift pattern is the regular working pattern a contract requires an employee to undertake in a periodic cycle in the course of the employee’s employment that specifies-

(a) the number of hours the employee must work over the course of the cycle before the next cycle begins, and

(b) the number of calendar days in the cycle over which the hours must be worked (including days on which the employee is not required to work) before the next cycle begins.

23.5 The relevant repeating shift pattern is that having effect in relation to the employee under the terms of a contract having effect at the end of the latest salary period ending on or before 19 March 2020.

23.6 In determining the usual hours of an employee in relation to a period of time, an hour that would otherwise be counted as a usual hour determined on the fixed hours basis in respect of an employee must not be excluded from the total number of the employee’s usual hours solely because that hour is-

(a) statutory payment leave as described in paragraph 19.6, or

(b) reduced rate paid leave as described in paragraph 19.7.

23.7 Paragraph 23.8 applies where-

(a) the first and last days of a CJRS claim period do not correspond exactly with the first and last calendar days of a single salary period,

(b) the making of a CJRS claim would be facilitated by the provision made by paragraph 23.8, and

(c) the amount of a CJRS claim determined in accordance with the facilitation permitted by paragraph 23.8 is not abusive or otherwise contrary to the purpose of CJRS.

23.8 Where this paragraph applies, the formula in paragraph 23.2 may be applied in respect of each salary period falling wholly or partly within the CJRS claim period as if CP referred to the number of calendar days covered by the salary period (or part thereof) falling within the CJRS claim period.

23.9 Where the formula in Paragraph 23.2 is used to determine the usual hours for a salary period falling wholly or partly within a CJRS claim period (“relevant part CJRS claim period”), the amounts determined in accordance with the formulae in paragraphs 16.3 and 16.4 in respect of all relevant part CJRS claim periods must be totalled for the purposes of determining the amount claimable for the CJRS claim period of the CJRS claim.

23.10 In respect of a relevant part CJRS claim period-

(a) paragraph 28.1 applies as if it provided that an amount of time that is less than an hour must be rounded up or down to the nearest whole number, and

(b) appropriate and proportionate adjustments must be made in respect of all matters relevant to determining the amount claimable in respect of the CJRS claim period of the CJRS claim so as to ensure the claim is not abusive or otherwise contrary to the purpose of CJRS.

CJRS claim period – usual hours – variable hours basis

24. The usual hours for a CJRS claim period in respect of an employee whose usual hours must be determined on the variable hours basis must be determined using the higher of-

(a) the averaging method (see, in particular, paragraphs 26.1 to 26.10), or

(b) the calendar look-back method (see, in particular, paragraphs 27.1 to 27.12).

CJRS claim period – usual hours – variable hours basis (relevant output work employee)

25.1 For the purposes of paragraphs 26.4(a), 27.4(a) and 27.8(a), an employee is a relevant output work employee if paragraph 25.2 applies in relation to an employee.

25.2 This paragraph applies in relation to an employee-

(a) whose contract provides for the employee to be paid by a measure of output by the worker (including a number of pieces made or processed or a number of tasks performed) which does not fall as time work within regulation 30 of the NMWR 2015, and

(b) whose employer does not know how many hours the employee works in any given period of time.

CJRS claim period – usual hours – variable hours basis (averaging method)

26.1 The formula in paragraph 26.2 applies to determine usual hours using the averaging method.

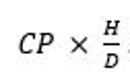

26.2 The formula referred to in paragraph 26.1 is-

26.3 For the purposes of paragraph 26.2-

(a) CP is the number of calendar days covered by the CJRS claim period;

(b) H is the number of relevant worked hours;

(c) D is the number of relevant employed days.

26.4 For the purposes of paragraph 26.3(b) an hour is a relevant worked hour if-

(a) the hour-

(i) falls, (in respect of a relevant output work employee), as an hour of output work (determined in accordance with Chapter 4 of Part 5 of the NMWR 2015) undertaken by the employee for the employer making the CJRS claim, or

(ii) in any other case, is an hour when the employee undertook paid work as an employee for the employer making the CJRS claim for that hour pursuant to a contract between the employer and the employee,

(b) the hour occurred in the tax year 2019/20, and

(c) the hour occurred before a time when the employee ceased all work in relation to their employment relevant for the making of a CJRS claim by the employer in respect of the employee in accordance with the original CJRS directions.

26.5 For the purposes of paragraph 26.3(c), a day is a relevant employed day if-

(a) the day is a day on which a contract between the employer making the CJRS claim and the employee has effect,

(b) the day occurred in the tax year 2019/20,

(c) the day occurred before a time when the employee ceased all work in relation to their employment as described in paragraph 26.4(c),

(d) the day does not fall in a period of statutory payment leave described in paragraph 19.6, and

(e) the day does not fall in a period of reduced rate paid leave described in paragraph 19.7.

26.6 For the purposes of paragraph 26.5(a), it does not matter if the employee undertook no work for the employer on that day.

26.7 Paragraph 26.8 applies where-

(a) the first and last days of a CJRS claim period do not correspond exactly with the first and last calendar days of a single salary period,

(b) the making of a CJRS claim would be facilitated by the provision made by paragraph 26.8, and

(c) the amount of a CJRS claim determined in accordance with the facilitation permitted by paragraph 26.8 is not abusive or otherwise contrary to the purpose of CJRS.

26.8 Where this paragraph applies, the formula in paragraph 26.2 may be applied in respect of each salary period falling wholly or partly within the CJRS claim period as if CP referred to the number of calendar days covered by the salary period (or part thereof) falling within the CJRS claim period.

26.9 Where the formula in paragraph 26.2 is used to determine the usual hours for a salary period falling wholly or partly within a CJRS claim period (“relevant part CJRS claim period”), the amounts determined in accordance with the formulae in paragraphs 16.3 and 16.4 in respect of all relevant part CJRS claim periods must be totalled for the purposes of determining the amount claimable for the CJRS claim period of the CJRS claim.

26.10 In respect of a relevant part CJRS claim period-

(a) paragraph 28.1 applies as if it provided that an amount of time that is less than an hour must be rounded up or down to the nearest whole number, and

(b) appropriate and proportionate adjustments must be made in respect of all matters relevant to determining the amount claimable in respect of the CJRS claim period of the CJRS claim so as to ensure the claim is not abusive or otherwise contrary to the purpose of CJRS.

CJRS claim period – usual hours – variable hours basis (calendar look-back method)

27.1 Where paragraph 27.3 applies, paragraph 27.4 applies to determine usual hours using the calendar look-back method.

27.2 Where paragraph 27.3 does not apply, paragraph 27.5 applies to determine usual hours using the calendar look-back method.

27.3 This paragraph applies when the first calendar day of a CJRS claim period and the last calendar day of that period correspond exactly with the first and last calendar days of a salary period in 2019.

27.4 Where this paragraph applies, the usual hours are-

(a) in relation to a relevant output work employee, the number of hours of output work (determined in accordance with Chapter 4 of Part 5 of the NMWR 2015) occurring in the salary period mentioned in paragraph 27.3;

(b) in any other case, the number of hours of relevant worked hours occurring in the salary period mentioned in paragraph 27.3.

27.5 Where this paragraph applies, the usual hours in respect of the CJRS claim period must be determined in accordance with the following steps-

(a) Step 1: the calendar days occurring in 2019 corresponding to the calendar days covered by the CJRS claim period (“the 2019 calendar days”) must be identified;

(b) Step 2: the salary periods occurring in 2019 that include one or more of the 2019 calendar days (“the 2019 salary periods”) must be identified;

(c) Step 3: the formula in paragraph 27.6 must be applied separately to each of the 2019 salary periods identified in step 2 to establish the number of usual hours referable to each of those salary periods;

(d) Step 4: the usual hours referable to each of the 2019 salary periods must be totalled to determine the number of usual hours for the purposes of the CJRS claim.

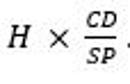

27.6 The formula referred to in paragraph 27.5(c) is-

27.7 For the purposes of paragraph 27.6-

(a) H is the number of relevant worked hours occurring in the 2019 salary period;

(b) CD is the number of 2019 calendar days occurring in the 2019 salary period;

(c) SP is the number of days covered by the 2019 salary period .

27.8 For the purposes of paragraph 27.7(a)-

(a) in relation to a relevant output work employee, an hour is a relevant worked hour if it is an hour of output work (determined in accordance with Chapter 4 of Part 5 of the NMWR 2015);

(b) in any other case, an hour is a relevant worked hour if the employee undertook paid work as an employee for the employer making the CJRS claim for that hour pursuant to a contract between the employer and the employee.

27.9 Paragraph 27.10 applies where-

(a) paragraph 27.5 applies to determine the usual hours in respect of the CJRS claim period,

(b) the making of a CJRS claim would be facilitated by the provision made by paragraph 27.10, and

(c) the amount of a CJRS claim determined in accordance with the facilitation permitted by paragraph 27.10 is not abusive or otherwise contrary to the purpose of CJRS.

27.10 Where this paragraph applies, paragraph 27.5 may be applied in respect of each salary period falling wholly or partly within the CJRS claim period as if-

(a) that paragraph made provision for determining the usual hours in respect of a salary period falling wholly or partly within a CJRS claim period,

(b) the reference in paragraph 27.5(a) to the calendar days covered by the CJRS claim period were a reference to the calendar days covered by the salary period, and

(c) paragraph 27.5(d) made provision for determining the number of usual hours for the number of calendar days covered by the whole or part of the salary period falling within the CJRS claim period.

27.11 Where paragraph 27.5 is applied as described in paragraph 27.10 to determine the usual hours for a salary period falling wholly or partly within a CJRS claim period (“relevant part CJRS claim period”), the amounts determined in accordance with the formulae in paragraphs 16.3 and 16.4 in respect of all relevant part CJRS claim periods must be totalled for the purposes of determining the amount claimable for the CJRS claim period of the CJRS claim.

27.12 Where paragraph 27.5 is applied as described in paragraph 27.10-

(a) paragraph 28.1 applies as if it provided that an amount of time (determined by reference to paragraph 27.5 applied as described in paragraph 27.10) that is less than an hour must be rounded up or down to the nearest whole number, and

(b) appropriate and proportionate adjustments must be made in respect of all matters relevant to determining the amount claimable in respect of the CJRS claim period of the CJRS claim so as to ensure the claim is not abusive or otherwise contrary to the purpose of CJRS.

CJRS claim period – usual hours – general provisions

28.1 If the number of usual hours determined in accordance with the fixed hours basis or the variable hours basis include an amount of time that is less than an hour, the number of usual hours must be rounded up to the next whole number.

28.2 In determining the usual hours of an employee in relation to a period of time on the fixed hours basis or the variable hours basis, an hour that would otherwise be counted as a usual hour in respect of the employee must not be excluded from the total number of the employee’s usual hours solely because that hour is-

(a) paid annual leave pursuant to regulation 16 of the Working Time Regulations 1998 or regulation 20 of the Working Time (Northern Ireland) Regulations 2016, or

(b) leave taken on account of time worked pursuant to a flexible work time arrangement. CJRS claim period – meaning of furloughed hours

29. The number of furloughed hours in a CJRS claim period relating to an employee must be determined by subtracting the number of hours the employee works in that period from the employee’s usual hours for that period.

Expenditure to be reimbursed

30. Subject as follows, on a claim by an employer for a payment under CJRS, the payment may reimburse-

(a) the gross amount of earnings paid or reasonably expected to be paid by the employer to an employee (subject to the maxima determined in accordance with paragraphs 31.1 to 31.4);

(b) the amount allowable as CJRS claimable employer national insurance contributions (see paragraphs 33.1 to 33.4);

(c) the amount allowable as a CJRS claimable pension contribution (see paragraphs 34.1 to 34.5).

Maximum gross earnings claimable

31.1 The amount to be paid to reimburse the gross amount of earnings must not exceed the lower of-

(a) the amount determined in accordance the with the formula in paragraph 16.3, and

(b) the amount determined in accordance the with the formula in paragraph 16.4.

31.2 Paragraphs 16.5 to 16.8 apply for the purposes of paragraph 31.1 subject to the modifications in paragraphs 31.3 and 31.4.

31.3 Where the CJRS claim period of a CJRS claim occurs in the CJRS calendar month of September 2020-

(a) paragraph 16.5(a)(i) applies as if the amount specified in that paragraph were £2,187.50 per month, and

(b) paragraph 16.5(b) applies as if the percentage specified in that paragraph were 70%.

31.4 Where the CJRS claim period of a claim occurs in the CJRS calendar month of October 2020-

(a) paragraph 16.5(a)(i) applies as if the amount specified in that paragraph were £1,875.00 per month, and

(b) paragraph 16.5(b) applies as if the percentage specified in that paragraph were 60%.

Statutory payments

32.1 No CJRS claim may include amounts of specified statutory payments in respect of an employee during the employee’s period of furlough and the gross amount of earnings falling for reimbursement as described in paragraph 31.1 must be correspondingly reduced.

32.2 The specified statutory payments for the purposes of paragraph 32.1 are-

(a) Statutory Maternity Pay pursuant to section 164 of SSCBA or section 160 of SSCB(NI)A;

(b) Statutory Adoption Pay pursuant to section 171ZL of SSCBA or section 167ZL of SSCB(NI)A;

(c) Statutory Paternity Pay pursuant to sections 171ZA and 171ZB of SSCBA or sections 167ZA and 167ZB of SSCB(NI)A;

(d) Statutory Shared Parental Pay pursuant to sections 171ZU and 171ZV of SSCBA or sections 167ZU and 167ZW of SSCB(NI)A;

(e) Statutory Parental Bereavement Pay pursuant to section 171ZZ6 of SSCBA or any provision made for Northern Ireland which corresponds to that section.

Employer national insurance contributions

33.1 An amount is allowable as CJRS claimable employer national insurance contributions only if the amount is referable to a CJRS claim period in July 2020.

33.2 The amount allowable as CJRS claimable employer national insurance contributions in respect of a CJRS claim period is the lower of-

(a) employer national insurance contributions payable by the employer in respect of the gross amount of earnings falling for reimbursement pursuant to the CJRS claim in respect of the CJRS claim period, and

(b) 13.8% of the gross amount of earnings falling for reimbursement pursuant to the CJRS claim in respect of the CJRS claim period that are-

(i) more than the secondary threshold relevant to the CJRS claim period, and

(ii) not more than the amount claimable by the employer in accordance with paragraph 30(a).

33.3 For the purposes of paragraph 33.2, the secondary threshold relevant to a CJRS claim period must be apportioned proportionately to reflect-

(a) the length of the CJRS claim period, and

(b) the number of the furloughed hours as are-

(i) within the CJRS claim period, and

(ii) proportionate to the number of usual hours falling within the CJRS claim period.

33.4 For the purposes of paragraphs 30. and 33.2-

(a) “employer national insurance contributions” are the secondary Class 1 contributions an employer is liable to pay as a secondary contributor in respect of an employee by virtue of sections 6 and 7 of the SSCBA or sections 6 and 7 of the SSCB(NI)A;

(b) “secondary threshold” means the secondary threshold (for secondary Class 1 contributions) for the purposes of section 5(1) of the SSCBA or section 5(1) of the SSCB(NI)A (see regulation 10 of the Social Security (Contributions) Regulations 2001) for the tax year ending on 5 April 2021.

CJRS claimable pension contributions

34.1 An amount is allowable as a CJRS claimable pension contribution only if the amount is referable to a CJRS claim period in July 2020.

34.2 The amount allowable as a CJRS claimable pension contribution in respect of a CJRS claim period is the lower of-

(a) the contribution payable by the employer to a registered pension scheme in respect of the gross amount of earnings falling for reimbursement pursuant to the CJRS claim in respect of the CJRS claim period, and

(b) 3% of the gross amount of earnings falling for reimbursement pursuant to the CJRS claim in respect of the CJRS claim period that is more than the lower limit for qualifying earnings (as set out in section 13 of the Pensions Act 2008).

34.3 For the purposes of paragraph 34.2, the lower limit for qualifying earnings in a CJRS claim period must be apportioned proportionately to reflect-

(a) the length of the CJRS claim period, and

(b) the number of furloughed hours as are-

(i) within the CJRS claim period, and

(ii) proportionate to the number of usual hours within the CJRS claim period.

34.4 For the purposes of paragraphs 34.1 to 34.3, “registered pension scheme” means a pension scheme for the purposes of Part 4 of the Finance Act 2004.

34.5 For the purposes of paragraphs 34.1 to 34.4 in relation to Northern Ireland, references to section 13 of the Pensions Act 2008 must be construed as references to section 13 of the Pensions (No. 2) Act (Northern Ireland) 2008.

Circumstances in which a CJRS claim may not be made

35. Where, during the period beginning on 1 July 2020 and ending on 31 October 2020, a period of unpaid sabbatical or other period of unpaid leave is taken by an employee (“unpaid leave”) no CJRS claim may be made in respect of the period of unpaid leave.

Further provision in relation to work for the purposes of CJRS

36.1 For the purposes of CJRS, an employee must be treated as working for an employer if the employee works for a person connected with the employer (see paragraph 41.4) or otherwise works indirectly for the employer.

36.2 Study or training undertaken must be disregarded for the purposes of paragraph 10.1 if-

(a) the purpose of the study or training is to improve-

(i) an employee’s effectiveness in the employer’s business, or

(ii) the performance of the employer’s business,

(b) except as generally improving an employee’s effectiveness in, or the performance of, an employer’s business, the study or training does not directly-

(i) provide a service to the employer or the business activities of the employer, or

(ii) contribute to the business activities of the employer or anything generating income or profit for the employer, and

(c) the study or training undertaken does not directly contribute to any significant degree-

(i) in the production of goods the employer intends to supply to another person as part of the making of a supply of goods or services for a consideration to that person, or

(ii) in the making to any person of a supply of services for a consideration by the employer.

36.3 References to “employer” in paragraphs 36.2 include a person connected with the employer.

36.4 In this paragraph and paragraphs 36.5 and 36.6-

(a) references to a scheme are references to anything falling as an occupational pension scheme by virtue of section 1 of the Pensions Schemes Act 1993 or section 1 of the Pensions Schemes (Northern Ireland) Act 1993;

(b) an employee is a trustee or manager of a scheme if the employee is a trustee or manager of the scheme determined in accordance with-

(i) in relation to England and Wales and Scotland, the Pensions Act 1995 (see, in particular, sections 124 and 176 of that Act), and

(ii) in relation to Northern Ireland, the Pensions (Northern Ireland) Order 1995 (see, in particular, articles 2 and 121 of that Order);

(c) a person who is a director of a company that is a trustee or manager of a scheme (determined in accordance with the legislation mentioned in paragraph 36.4(b) must be treated as if that person were a trustee or manager of the scheme;

(d) a person who is an employee of a company treated as a trustee or manager of a scheme by virtue of paragraph 36.4(c) must be treated as if that person were a trustee or manager of the scheme;

(e) whether a person is an independent trustee of a scheme must be determined in accordance with section 23(3) of the Pensions Act 1995.

36.5 Work undertaken by an employee for the sole purpose of fulfilling their duties as a trustee or manager of a scheme must be disregarded for the purposes of paragraph 10.1.

36.6 Work is not undertaken by an employee for the sole purpose of fulfilling their duties as a trustee or manager of a scheme if-

(a) the work undertaken by the employee is for the purpose of fulling their duties as an independent trustee of the scheme, and

(b) the business activities of the employee’s employer include-

(i) the provision of services as a trustee or manager of the scheme, or

(ii) requiring the employee (whether solely or together with other duties or responsibilities) to undertake duties as an independent trustee of the scheme.

36.7 Work undertaken by a director of a company must be disregarded for the purposes of paragraph 10.1 if the work undertaken directly relates to-

(a) fulfilling a duty or other obligation arising by or under an Act of Parliament relating to the filing of company accounts or provision of other information relating to the administration of the director’s company,

(b) making a CJRS claim in respect of an employee of the director’s company, or

(c) making a payment of salary or wages of an employee of the director’s company.

36.8 For the purposes of paragraph 36.4(e) in relation to Northern Ireland, the reference to section 23(3) of the Pensions Act 1995 must be construed as a reference to article 23.3 of the Pensions (Northern Ireland) Order 1995.

Succession to a business – new employer is not a qualifying employer

37.1 A new employer may make a CJRS claim in respect of an employee who is a relevant transferred employee by virtue of paragraph 37.4(a) or paragraph 37.4(b) as if the new employer had-

(a) a qualifying PAYE scheme, and

(b) made a payment of earnings in respect of the relevant transferred employee in the tax year 2019-20 which is shown in a return under Schedule A1 to the PAYE Regulations made on or before 19 March 2020.

37.2 A new employer may make a CJRS claim in respect of an employee who is a relevant transferred employee by virtue of paragraph 37.4(c) or paragraph 37.4(d) as if-

(a) the new employer had-

(i) a qualifying PAYE scheme,

(ii) made a payment of earnings in respect of the relevant transferred employee in the tax year 2019-20 which is shown in a return under Schedule A1 to the PAYE Regulations made on or before 19 March 2020, and

(iii) made a qualifying CJRS claim (see paragraph 8.3), and

(b) paragraph 10.3 applies in relation to the employee.

37.3 An employer is a new employer for the purposes of CJRS if the employer’s PAYE scheme is not a qualifying PAYE scheme solely because the employer’s PAYE scheme was registered on HMRC’s real time information for PAYE after 19 March 2020.

37.4 An employee is a relevant transferred employee-

(a) if-

(i) paragraph 10.3 applies in relation to the employee by virtue of a CJRS claim in accordance with the original CJRS directions made by the new employer, and

(ii) paragraph 37.5 applies in relation to the employee;

(b) if-

(i) paragraph 10.3 applies in relation to the employee by virtue of a CJRS claim in accordance with the original CJRS directions made by the new employer, and

(ii) paragraph 37.7 applies in relation to the employee;

(c) if-

(i) paragraph 37.5 (as modified by paragraph 37.11 for the purposes of this paragraph) applies in relation to the employee, and

(ii) paragraph 37.13 applies in relation to the employee; or

(d) if-

(i) paragraph 37.7 (as modified by paragraph 37.12 for the purposes of this paragraph) applies in relation to the employee, and

(ii) paragraph 37.13 applies in relation to the employee.

37.5 This paragraph applies in relation to an employee if-

(a) on 28 February 2020 the employee was employed by an employer (“former employer”) who is not the new employer,

(b) after 28 February 2020, there is a change in the employee’s employer from the former employer to the new employer while the employee remains in employment in the same business,

(c) immediately before the change, the former employer’s PAYE scheme having effect in relation to the employee was a qualifying PAYE scheme, and

(d) any of the circumstances in paragraph 37.6 apply.

37.6 The circumstances referred to by paragraph 37.5(d) are-

(a) regulation 102 of the PAYE Regulations has effect so that the change of employer from the former employer to the new employer is not to be treated as a cessation of employment for the purposes of regulation 36 of those Regulations (cessation of employment: Form P45);

(b) the transfer of the business or undertaking (or part thereof) resulting in the change in the employee’s employer from the former employer to the new employer does not operate so as to terminate the contract of employment of the employee by virtue of the Transfer of Undertakings (Protection of Employment) Regulations 2006 (“TUPE”);

(c) the transfer of the trade, business or undertaking resulting in the change in the employee’s employer from the former employer to the new employer does not operate so as to break the continuity of the period of employment of the employee by virtue of section 218 of the Employment Rights Act 1996.

37.7 This paragraph applies in relation to an employee if-

(a) on 28 February 2020, the employee was employed by an employer (“former employer”) who is not the new employer,

(b) in the period beginning on 1 March 2020 and ending on 30 June 2020, the employee’s employment with the former employer is terminated before the time of the relevant transfer,

(c) the sole or principal reason for the termination of the employee’s employment is the relevant transfer,

(d) the sole or principal reason for the employee’s employment by the new employer is the relevant transfer,

(e) the employee’s employment by the new employer begins on the day when the employee’s employment with the former employer is terminated,

(f) immediately before the termination of the employee’s employment, the former employer’s PAYE scheme having effect in relation to the employee was a qualifying PAYE scheme, and

(g) paragraph 37.8 applies in relation to the employee’s former employer.

37.8 This paragraph applies in relation to an employee’s former employer if-

(a) regulations 4 and 7 of TUPE do not apply in relation to the relevant transfer only by virtue of regulation 8(7) of TUPE, and

(b) at the time of the relevant transfer, a winding-up order has been made in respect of the former employer pursuant to Chapter 6 of Part 4 of the Insolvency Act 1986.

37.9 For the purposes of paragraphs 37.7, 37.8, and 37.14 to 37.16, “relevant transfer” means a transfer of a business or undertaking (or part thereof) resulting in the change in the employee’s employer from the former employer to the new employer that falls as a “relevant transfer” for the purposes of TUPE.

37.10 In relation to Northern Ireland-

(a) the reference in paragraph 37.6(c) to section 218 of the Employment Rights Act 1996 must be construed as a reference to article 14 of the Employment Rights (Northern Ireland) Order 1996, and

(b) the reference in paragraph 37.8(b) to Chapter 6 of Part 4 of the Insolvency Act 1986 must be construed as a reference to Chapter 6 of Part 5 of the Insolvency (Northern Ireland) Order 1989.

37.11 The modifications to paragraph 37.5 for the purposes of paragraph 37.4(c)(i) are that-

(a) paragraph 37.5(a) must be construed as referring to 10 June 2020 and not 28 February 2020, and

(b) paragraph 37.5(b) must be construed as referring to 10 June 2020 and not 28 February 2020.

37.12 The modifications to paragraph 37.7 for the purposes of paragraph 37.4(d)(i) are that-

(a) paragraph 37.7(a) must be construed as referring to 10 June 2020 and not 28 February 2020, and

(b) paragraph 37(7)(b) must be construed as if the period mentioned in that paragraph were the period beginning on 11 June 2020 and ending on 31 October 2020.

37.13 This paragraph applies in relation to an employee if-

(a) the employee’s former employer falls as a qualifying employer in relation to the employee, and

(b) the employee falls as a qualifying employee in relation to the former employer.

37.14 For the purposes of paragraph 37.13-

(a) references to a former employer falling as a qualifying employer include a person who would do so if the relevant transfer had not occurred, and

(b) references to an employee falling as a qualifying employee include a person who would do so if the relevant transfer had not occurred.

37.15 For the purposes of determining the number of allowable claimed-for employees for a CJRS claim made in respect of a CJRS period that includes a day falling on or after the day of a relevant transfer-

(a) an employee who, by reason of that relevant transfer, is a relevant transferred employee by virtue of paragraph 37.4(c) or paragraph 37.4(d) must be treated as a returning employee for the purposes of paragraphs 15.1 to 15.13, and

(b) the relevant transfer by which that employee became a relevant transferred employee must be treated as that employee’s return to work day for the purposes of those paragraphs.

37.16 For the purpose of a CJRS claim by a new employer in relation to an employee who is a relevant transferred employee by virtue of paragraph 37.4(c) or paragraph 37.4(d)-

(a) paragraphs 14.1 to 14.10 apply as if paragraph 14.8 allowed an initial CJRS claim to be made in respect of a period of no more than 6 consecutive days beginning on the day immediately following the day of the relevant transfer (subject to the making of a further CJRS claim in respect of the employee as described in that paragraph), and

(b) this direction and the original CJRS directions must be construed with such modifications as are necessary to facilitate the claim consistently with the purpose of CJRS.

37.17 For the purpose of determining a CJRS claim by a former employer in relation to an employee who is a relevant transferred employee by virtue of paragraph 37.4(c) or paragraph 37.4(d), paragraph 14.3(b) applies as if it also referred to the day immediately preceding the day of the relevant transfer.

37.18 In paragraph 37.17, the reference to “relevant transfer” is a reference to-

(a) an event by which an employee’s employer changes from a former employer to a new employer in respect of an employee who is a relevant transferred employee because paragraph 37.5 applies in relation to the employee;

(b) an event that falls as a relevant transfer described in paragraph 37.9 in respect of an employee who is a relevant transferred employee because paragraph 37.7 applies in relation to the employee.

Succession to a business – new employer already has a qualifying PAYE scheme

38.1 Paragraph 38.2 applies in a case where an employer is unable to make a CJRS claim pursuant to paragraphs 37.1 to 37.16 solely because the employer has a qualifying PAYE scheme.

38.2 Where this paragraph applies, a CJRS claim (subject to fulfilling all other requirements for making a CJRS claim) may be made-

(a) in relation to an employee falling as a relevant transferred employee by virtue of paragraphs 37.4(a) to 37.4(d), as if the employer had made a payment of earnings in respect of the relevant transferred employee in the tax year 2019-20 which is shown in a return under Schedule A1 to the PAYE Regulations that is made on or before 19 March 2020, and

(b) in relation to an employee falling as a relevant transferred employee by virtue of paragraph 37.4(c) or paragraph 37.4(d), as if-

(i) the employer had made a qualifying CJRS claim (see paragraph 8.3), and

(ii) paragraph 10.3 applies in relation to the employee.

38.3 Paragraphs 37.15 to 37.18 apply in relation to an employee in respect of whom a CJRS claim may be made pursuant to paragraph 38.2.

PAYE scheme reorganisations

39.1 A PAYE scheme registered on HMRC’s real time information system for PAYE after 28 February 2020 (“new scheme”) is a qualifying PAYE scheme if-

(a) the purpose of the new scheme is to replace at least two (but not necessarily all) of the employer’s qualifying PAYE schemes (“the transferred schemes”) in consequence of a reorganisation of the employer’s business, and

(b) the new scheme only has effect in relation to employees who are former members of one of the transferred schemes before the new scheme has effect in relation to any other employee.

39.2 An employee is a former member of one of the transferred schemes if-

(a) the new scheme has effect in relation to the employee, and

(b) one of the transferred schemes has effect in relation to the employee immediately before the new scheme has effect in relation to the employee.

39.3 Where a new scheme is a qualifying PAYE scheme by virtue of paragraph 39.1, a payment of earnings to a former member of one of the transferred schemes in the tax year 2019-20 which is shown in a return under Schedule A1 to the PAYE Regulations made on or before 19 March 2020 in respect of one of the transferred schemes must be treated as if the new scheme had effect in relation to the payment of earnings and had been shown in a return under Schedule A1 to the PAYE Regulations made on or before 19 March 2020 in respect of the new scheme.

Duration of CJRS in accordance with Part 2 of the Schedule to this direction

40. CJRS in accordance with Part 2 of the Schedule to this direction has effect only in relation to-

(a) amounts of earnings paid or payable by employers to flexibly-furloughed employees in respect of the period beginning on 1 July 2020 and ending on 31 October 2020, and

(b) employer national insurance contributions and CJRS claimable pension contributions paid or payable in relation to earnings paid or payable by employers to flexibly-furloughed employees in respect of the period beginning on 1 July 2020 and ending on 31 July 2020.

Definitions etc.

41.1 For the purposes of CJRS-

(a) a day is a relevant CJRS day if that day is-

(i) 28 February 2020, or

(ii) 19 March 2020;

(b) references to a “day” are references to a calendar day unless the context otherwise requires;

(c) references in part 2 of this Schedule to-

(i) a “CJRS claim” are references to a claim made in accordance with part 2 of this Schedule unless the context requires the reference to be construed as a reference to a claim made in accordance with the original CJRS directions;

(ii) a “CJRS claim period” are references to a claim period meeting the requirements of paragraphs 14.1 to 14.10 of this Schedule unless the context requires the reference to be construed as a reference to a period in respect of a CJRS claim made in accordance with the original CJRS directions;

(iii) a “salary period” are references to a salary period occurring wholly or partly within a CJRS claim period unless the context otherwise requires;

(d) references in part 2 of this Schedule to the “original CJRS directions”-

(i) are references to the direction (“first CJRS direction”) made on 15 April 2020 by the Treasury in exercise of the powers conferred by sections 71 and 76 of the Coronavirus Act 2020 as modified by the second CJRS direction, and

(ii) where necessary, must be construed as references to the first CJRS direction before its modification by the second CJRS direction;

(e) “charity” has the same meaning as it does in section 18 of the Small Charitable Donations Act 2012 (“SCDA”);

(f) “collective agreement” has the meanings given by section 178(1) and (2) of the Trade Union and Labour Relations (Consolidation) Act 1992 in relation to England and Wales and Scotland and Article 2(2) of the Industrial Relations (Northern Ireland) Order 1992 in relation to Northern Ireland;

(g) “company” has the same meaning as it does for the purposes of the Corporation Tax Acts set out in section 1121 of the Corporation Tax Act 2010 (“CTA”);

(i) “earnings” has the same meaning as it does in the employment income Parts of the Income Tax (Earnings and Pensions) Act 2003 (“ITEPA”) by virtue of section 62 of that Act;

(j) “employment” and corresponding references to “employed”, “employer” and “employee” have the same meanings as they do in section 4 of ITEPA as extended by-

(i) section 5 of that Act,

(ii) regulation 10 of the PAYE Regulations (application to agencies and agency workers), and

(iii) paragraphs 41.2 and 41.3 of this direction;

(k) “HMRC” means Her Majesty’s Revenue and Customs;

(l) “NMWR 2015” means the National Minimum Wage Regulations 2015;

(m) “PAYE” means pay as you earn;

(n) “PAYE Regulations” means the Income Tax (Pay As You Earn) Regulations 2003;

(o) “second CJRS direction” means the direction made on 20 May 2020 by the Treasury in exercise of the powers conferred by sections 71 and 76 of the Coronavirus Act 2020;

(p) “SSCBA” means the Social Security Contributions and Benefits Act 1992;

(q) “SSCB(NI)A” means the Social Security Contributions and Benefits (Northern Ireland) Act 1992;

(r) “statutory sick pay” means statutory sick pay payable pursuant to section 151 of the SSCBA or section 147 of the SSCB(NI)A;

(s) “trade union” has the meanings given by section 1 of the Trade Union and Labour Relations (Consolidation) Act 1992 in relation to England and Wales and Scotland and Article 3(1) of the Industrial Relations (Northern Ireland) Order 1992 in relation to Northern Ireland.

41.2 Where, by virtue of section 61R of ITEPA (workers services provided to the public sector through intermediaries), the Income Tax Acts apply as if a worker were employed by an employer, the worker is treated for the purposes of the CJRS as an employee of the person who is the deemed employer in relation to the worker by virtue of that section (and, in particular, amounts treated as earnings are treated as earnings for those purposes).

41.3 Where, by virtue of section 863A of the Income Tax (Trading and Other Income) Act 2005 (limited liability partnerships: salaried members), a person (“P”) is treated for the purposes of the Income Tax Acts as being employed by a limited liability partnership (“E”) under a contract of service instead of being a member of the partnership-

(a) P is treated as an employee for the purposes of CJRS, and

(b) E is treated as P’s employer for the purposes of CJRS.

41.4 For the purposes of determining whether a person, company or charity is connected with an employer for the purposes of CJRS-

(a) whether a person is connected with an employer must be determined in accordance with section 993 of the Income Tax Act 2007;

(b) without prejudice to paragraphs 41.4(a) and 41.4(c), whether a company is connected with an employer (where the employer is a company) must be determined in accordance with section 1122 of CTA;

(c) without prejudice to paragraphs 41.4(a) and 41.4(b), whether a charity is connected with an employer (where the employer is a charity) must be determined in accordance with section 5 of SCDA construed as if-

(i) references to a tax year in that section were omitted, and

(ii) subsection (7) of that section were omitted.

Other directions under section 76 of the Coronavirus Act 2020

42.1 HMRC must take account of any amendment made to CJRS by any other direction under section 76 of the Coronavirus Act 2020.

42.2 Entitlement to a payment under CJRS is without prejudice to any entitlement to a payment under any similar scheme arising from a direction under section 76 of the Coronavirus Act 2020.

HMRC’s accounts

43. CJRS payments made by HMRC must be shown in HMRC’s consolidated accounts produced for the purposes of section 6(4) of the Government Resources and Accounts Act 2000 and section 2 of the Exchequer and Audit Departments Act 1921 for the year ending on 31 March 2021.